The Office of Sponsored Programs

The Office of Sponsored Programs (OSP) supports faculty and staff throughout the grant life cycle, from initial interest in pursuing a grant, through compliant administration, all the way to grant closeout. Sponsored Programs at Belmont may be in support of faculty research and scholarly agendas, program and curricula development, and other college or faculty-initiated projects. Faculty and staff members who are interested in pursuing external grant opportunities are encouraged to contact osp@belmont.edu in the Office of Sponsored Programs prior to seeking external funding. OSP can provide technical assistance and coordination support for every step of your application process.

Prior to Grant Submission

The Office of Sponsored Programs:

- Identifies grant opportunities

- Obtains and interprets grant guidelines

- Assists in developing a budget

- Advises potential applicants on gaining required internal endorsements

- Advises on the completion of sponsor forms and certifications

- Assists with letters of intent, preliminary proposals, and teaming agreements

- Assists with navigating government grant submission platforms like grants.gov and research.gov

Once a grant is ready to be submitted, OSP has the authority to submit electronic proposals on behalf of the University.

Once the Grant is Awarded

The Office of Sponsored Programs:

- Reviews and negotiates grant terms and contract clauses on behalf of the University

- Facilitates the establishment of award accounts in the University system

- Oversees project activity in partnership with the Project Director and the Office of the Controller to ensure compliance with the policies of the sponsor and the University

Belmont Grant Recipients

BRIDG Grant Awardees

The Office of Sponsored Programs is proud to announce the recipients of the 2026 BRIDG Grants. Created to support innovative ideas, pilot projects, and emerging research initiatives, the BRIDG Grant Program provides funding opportunities for faculty and staff who are new to grant-funded work or early in their careers.

On May 1, 2026, 11 BRIDG grants were awarded to 13 faculty members from across Belmont University's colleges and disciplines, advancing projects that will enrich scholarship, creativity, and innovation throughout the Belmont community.

Recipients and Projects

Proposal Title: Curiosity Lab: Exploring creativity and belonging in an AI-immersed landscape

Proposal Title: Curiosity Lab: Exploring creativity and belonging in an AI-immersed landscape

The Creative Inquiry Researcher advances Belmont's mission to empower students as creative problem solvers and compassionate leaders. This project provides future classroom teachers with hands-on research experience, close faculty mentorship, and experience implementing in the field, which are all hallmarks of NSSE's High-Impact Practices.

As AI reshapes classrooms and workplaces, empirical data related to implementation in classrooms is needed. This project highlights Belmont's commitment to AI innovation as well as student belonging and purpose. It also aligns with NACE’s call for meaningful, paid experiential learning that prepares students for the future workforce.

Proposal Title: Cultivating grit through Occupation: A Pilot Leisure-Based Intervention with Occupational Therapy Students

This BRIDG project supports Belmont’s commitment to holistic student development by exploring an innovative, occupation-based approach to enhancing student grit and well-being. The findings may inform future student success and well-being programming while contributing new evidence to occupational therapy education.

Proposal Title: Predictors of High Compliance-Related Stress in Prelicensure Nursing Students: A Pilot Study

My BRIDG project investigates what puts nursing students at greatest risk for high compliance-related stress, the administrative burden of immunizations, certifications, screenings, and documentation required before clinical placements. Building on a prior study where I developed a new measurement tool and identified three distinct stress profiles among Belmont nursing students, this follow-up study will test whether those patterns hold in a new cohort and pinpoint the factors that predict which students are most affected. The goal is to generate evidence that helps Belmont better support students through a demanding but understudied part of their training, while producing a research tool other nursing programs nationwide can use.

Proposal: Elucidating the Mechanism of Digitoxin-Mediated Decreases in Triple Negative Breast Cancer Cell Viability

My BRIDG project provides students with hands-on experience in basic medical research, introducing many to laboratory research for the first time. The project focuses on investigating drug repurposing as a potential treatment for breast cancer, giving students the opportunity to contribute to research with real-world significance. BRIDG funding supports the purchase of essential drugs and laboratory reagents needed to conduct experiments. Through this experience, students see how they can make an impact on the world from a scientific perspective.

Proposal: Music in the Redwoods

Faculty research always informs the classroom experience in unexpected ways, from new history learned to anecdotes about the research experience to learning about the research process. This project in particular is going to be used in my graduate Introduction to Research class to talk about the joys of serendipity in research (these materials are a true rare find), archival work, digitizing sources, applying for grants, and more. And in my undergraduate music history survey classes, my work on the Grove Play as a little-known form of American musica secreta will support my daily goal of connecting music to real life and societal movements.

Proposal: Advancing AI Monitoring and Oversight Competencies in PharmD Education: A Workforce and Strategic Readiness Pilot

Artificial intelligence is rapidly becoming part of healthcare, creating new opportunities as well as new responsibilities for pharmacists. National healthcare regulators, pharmacy organizations, and pharmacy educators increasingly recognize that future pharmacists must be able to evaluate AI-generated information and verify its accuracy before using it to support patient care. This BRIDG-funded project will help Belmont pharmacy students develop those skills by working with real healthcare datasets, comparing AI-generated answers to validated data, and learning how to identify errors and limitations in emerging technologies. By combining pharmacy, data analytics, and artificial intelligence in a hands-on learning environment, Belmont is preparing graduates to lead in a rapidly changing healthcare landscape while helping ensure the safe and responsible use of AI in patient care.

Proposal: Defining the BRCA-1-NRF2 Transciptional Axis as a Therapeutic Vulnerability in Triple-Negative Breast Cancer

This BRIDG award will fund stipends for five students in SURVIVE (Summer Undergraduate Research and Visualization in Investigative and Vital Experiences), an intensive summer research training program created by Dr. Jamaine Davis at the Thomas F. Frist, Jr. College of Medicine. Students are placed in faculty-mentored computational biology projects examining how variation in genes and proteins translates into measurable differences in cancer biology, drug sensitivity, and patient survival, with faculty from Belmont Frist College of Medicine along with investigators from Meharry Medical College guiding instruction. Each student will submit a first-author, peer-reviewed manuscript within six months of completing the program — Belmont will appear in those author affiliations, expanding the institution's scholarly footprint in the biomedical literature at a critical moment in the Frist College of Medicine's development — strengthening partnerships with minority-serving institutions in the Nashville research corridor and advancing LCME accreditation standards. SURVIVE reflects a deliberate investment in the training of physician scholars, giving medical students the tools, mentorship and hands-on experience to engage in translational research early in their training.

Proposal: The Last Note: Final Performances of Legendary Pianists

This project will make an impact at Belmont by offering a different model for learning music literature—one rooted not only in facts, dates, and repertoire, but in the dignity and complexity of human lives. This book explores the final performances of fifty major pianists, using archival research to tell the human stories behind the public moments, e.g., artists facing illness, aging, reinvention, personal loss, and the human desire to communicate something of worth through their art. The project reflects Belmont’s commitment to the dignity and worth of every person by asking students and readers to encounter historical subjects not as distant names in a textbook, but as whole human beings. The BRIDG grant supports the final stages of this project which hopes to bring scholarship into conversation with empathy and creativity.

Proposal: Religion and Spirituality in Play Therapy Practice: A Pilot Survey of Registered Play Therapists in Tennessee and Texas

Proposal: Neuro-Labeling the Curriculum: Validating Cognitive Demands of K-12 Textbooks thorugh Multimodal fNIRS and Physiological Stress Profiling in University Freshmen

Proposal: The Vocal Athlete's Wellness: Integrating Physical Therapy and Vocal Performance

Federal Notices

FAQ's Regarding Indirect Costs

Key Points:

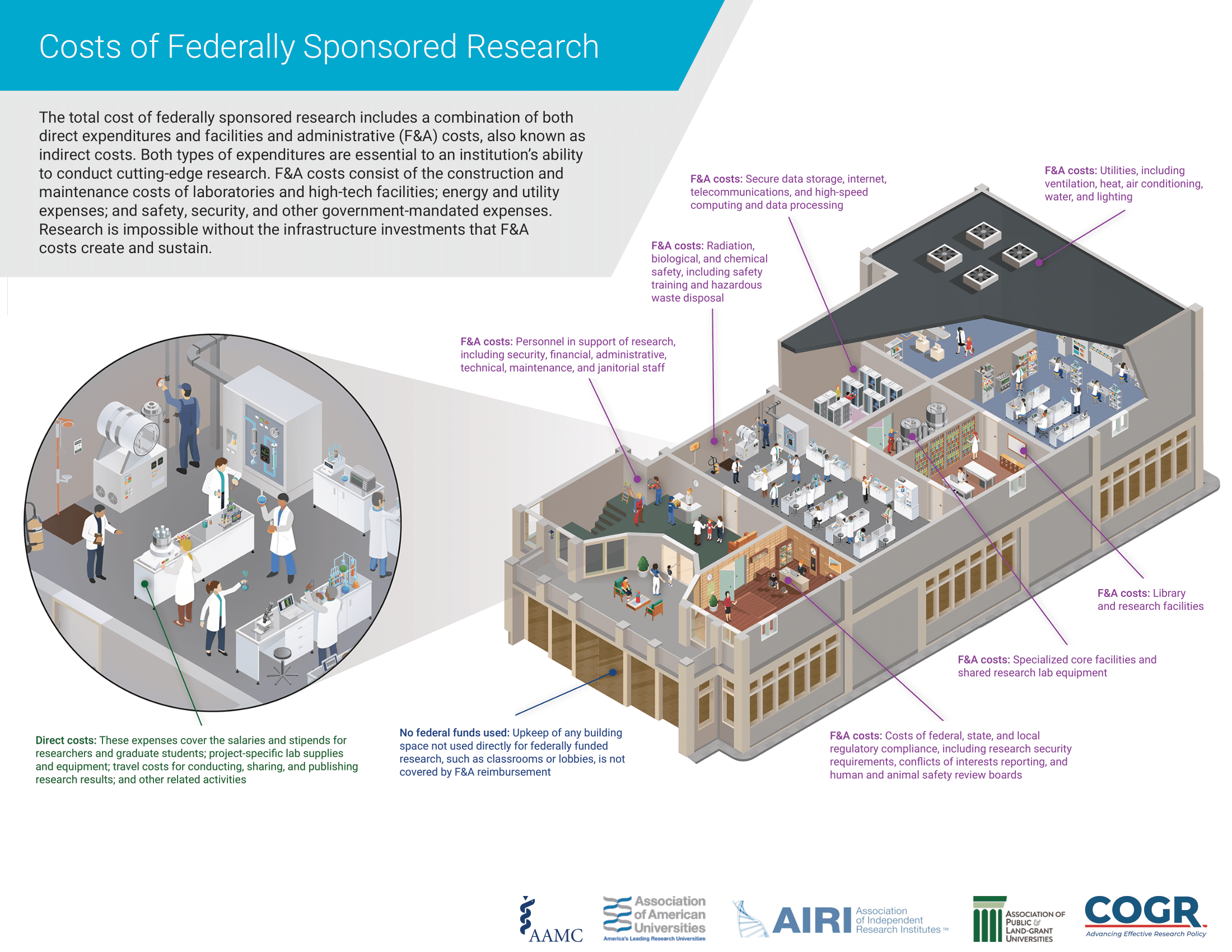

- F&A costs – also referred to as ‘indirect costs’ – are an essential part of the total costs of research and are necessary for safely, securely, efficiently, and effectively conducting world-leading research. Unlike the direct costs of research, such as project-specific research salaries and supplies, F&A costs are not easily assignable at the project level.

- F&A expenses include costs of building and maintaining state-of-the art research laboratories, facilitating high-speed data processing, compliance with national security protections (e.g., export controls, cybersecurity, research data security), patient safety protocols (e.g., human subjects protections); radiation safety and hazardous waste disposal; personnel required to support essential administrative and regulatory compliance work, maintenance staff, and other activities necessary for supporting research.

- The federal government reimburses an institution an agreed-upon proportion of the F&A costs the institution incurred to conduct research based upon the F&A cost reimbursement rates it negotiated with the institution.

- F&A cost reimbursement estimates are provided in the budgets of the future federal grants received by the institution but F&A cost reimbursement rates are only applied/charged to federal projects as direct project costs are charged.

Examples from Institution Websites

- “Facilities & Administrative (F&A) costs, also known as indirect costs or institutional overhead, are expenses that support the overall infrastructure and administration of research projects but cannot be directly attributed to any specific project. They include shared services such as: libraries, physical plant operation and maintenance, utility costs, departmental and sponsored project administrative expenses, depreciation or use allowance for buildings and equipment. F&A costs are a reimbursement to the institution for costs already incurred in supporting research activities. However, these reimbursements do not cover the entire cost of conducting research.” – The University of Iowa

- “Facilities and administration costs are general in nature, shared by multiple users, where it is not easy to determine each user’s share. F&A costs include electricity, water, utilities, and administrative research services. Direct costs can be assigned to a specific project with a high degree of accuracy. Direct costs include faculty, technical and student salary, ERE, travel, scientific supplies, equipment, tuition, human subject incentives, animal costs and consultant pay.” – Arizona State University

- “Facilities and administrative (F&A) costs are costs that are not readily identifiable with individual projects or, put another way, "those that are incurred for common or joint objectives." In other words, indirect costs cannot be specifically attributed to an individual project. For example, it is difficult to say how much of a PI's lab space is used for a specific research project when multiple projects are being conducted in the same lab. We know the project benefits from the lab space, but it is impractical to accurately calculate the cost associated with that benefit. Accordingly, F&A costs are estimated for each project using a formula that compares all Institutional project expenditures against all the Institutional facility and administrative costs necessary to support all projects. They include such categories as library operations, utility costs, depreciation of buildings and equipment, operations and maintenance costs, grant and contract administration and accounting, and general administrative expenses for central offices. Whatever we call them, indirect costs are real. The University is dependent upon the recovery of F&A costs in order to maintain the infrastructure necessary to support sponsored activities. Faculty, staff, and students involved in research and sponsored programs experience the benefits of F&A cost recovery every day when they enter a building, turn on the lights, consult with a research assistant, get help from research administration professionals when they write proposals or in managing grants and contracts, or use the telephone, internet or the libraries just to name a few examples.” – The University of Utah

Key Points

- F&A cost reimbursement rates are established in accordance with prescriptive federal guidelines and based on the university’s costs already incurred, and documented in the university’s financial statements and systems. F&A rates are determined in negotiation with a lead federal agency on a regular basis for a particular amount of time. In principle, the calculation is as follows:

- (Facilities costs + Administrative costs)/Modified Total Direct Costs

- Some large expenses, such as equipment, tuition remission, and the majority of subaward costs, are removed from Direct costs for rate calculation and application purposes, leaving only Modified Total Direct Costs (MTDC) and resulting in a more equitable distribution of F&A costs among activities.

- For Institutions of Higher Education, the administrative portion of the rate is reduced to 26%. A University with a 24% facilities component and a 30% administrative component can, therefore, only propose a 50% total rate.

- The rate is not the percentage of total project costs attributable to F&A.

- For example, if an institution has a rate of 50% and MTDC of $100,000, the F&A costs charged to the project will be $50,000. Therefore, with a rate of 50%, no more than 1/3 ($50,000/$150,000) of the project funding is charged as F&A costs.

- Direct cost items not included in MTDC further reduce the ratio of F&A cost reimbursement to total project cost.

• Universities and the federal government will often negotiate different reimbursement rates for: sponsored research conducted on campus, sponsored research conducted off campus, instruction, and other non-research related sponsored programs, further ensuring the reasonableness of the rates charged.

Text Examples for Institution Websites

• “4. How is the overall F&A cost rate calculated? A formalized process developed by the Federal government (consistent with generally accepted accounting principles and presented in 2 CFR part 200) is used to determine the University's F&A cost rate for sponsored research. First, all F&A costs within the institution are assigned to one of nine cost pools related to primary functions. 2 CFR part 200 defines the nine cost pools (see Section 5). Then a fractional amount from each cost pool is attributed to the research enterprise according to guidelines provided in 2 CFR part 200. Totaling these fractional dollar amounts yields the University's total F&A costs (TFAC) attributable to sponsored research. The TFAC total is then converted to an F&A cost rate by dividing it by "Modified Total Direct Costs" (MTDC).” – University of Cincinnati

• “To determine the level of F&A expenses the federal government will cover, every 2 to 4 years, the agency responsible for setting a university’s F&A cost rate (either the Department of Defense Office of Naval Research or the Department of Health and Human Services) will comprehensively audit and/or assess these shared costs to determine the appropriate federal reimbursement rate based upon specific costs that have been deemed allowable expenses by the OMB. The reimbursement rate is a percentage of a subset of direct research costs (not a percentage of total award). Some direct research costs (like equipment, capital expenditures, charges for patient care, rental costs, tuition remission, and scholarships and fellowships) are excluded from the direct cost for F&A cost calculation purposes. This remaining amount is known as modified total direct cost (MTDC). For example, after reviewing the costs of a university’s research projects during a base year, and considering anticipated changes such as increases in MTDC, a university and the federal government may determine that an amount equal to 50 percent of research MTDC is appropriate for the federal government to contribute toward F&A expenses. In that case, if the federal government awards a university $450,000 for the direct research portion of a grant, of which $365,000 is the modified total direct cost, then it also awards $182,500 for F&A cost reimbursements, for a total of $632,500. These overall institutional F&A cost rates are applied uniformly to each research grant as its direct funds are spent, avoiding the very tedious, expensive and inefficient process of computing the F&A expenses for individual awards – which would add additional costs for both the government and the university.”

– Association FAQs about F&A Costs of Federally Sponsored Research

Key Points

- The federal agency responsible for setting a university’s F&A cost reimbursement rate (for most universities either the Department of Defense Office of Naval Research or the Department of Health and Human Services) will comprehensively review the university’s rate proposal. It will confirm that federal guidelines have been followed, unallowable expenses and activities that do not benefit federal research (e.g. fundraising) have been removed from proposed F&A costs, and chosen allocation methods are reasonable and in accordance with the prescribed methodology. The federal agency will require adjustments if any problems are found and may further reduce rates if it considers them unreasonable (e.g. if they have increased significantly from the last negotiated rates).

Text Example for Institution Websites

- “6. What is the administrative process for negotiating the final F&A cost rate? Once the F&A cost information is assembled and appropriately documented, it is submitted to the Department of Health and Human Services (DHHS), which is the University's cognizant federal agency. DHHS negotiators from the Division of Cost Allocation for the Central States Field Office in Dallas make their own evaluation of the materials submitted and seek to negotiate downward some of the costs included in the pools Another (lower) rate is established for off-campus research (26.0%), for which some of the underlying costs such as building rental are charged directly to the grant and not borne as an F&A cost by the University. As has already been noted, the Federal government imposes selective restrictions on the F&A costs attributed to certain grants, such as the 8% rate on many training grants."" and “7. What expenses are not allowable in cost pools according to the Uniform Cost Principles? Much of the public discussion of F&A costs in the early 90's focused on the four cost pools categorized as ""Administration,"" in part because the guidelines in Circular A-21 were often ambiguous with respect to expenditures allowed in this category. Whereas a number of administrative expenditures had been allowed before the intense scrutiny in 1991, new allowability standards were applied retroactively. In the climate of the mid 90's, it was no longer a question of whether an expenditure has been allowed by Circular A-21, but whether it is considered reasonable by current standards. In the turbulent atmosphere generated by congressional investigations, previous "unallowables" were made more explicit and new ones were added.” – University of Cincinnati

- “Universities are mindful of the need to appropriately use federal resources and contain costs while getting the most from each research project. In fact, it is worth noting that the F&A portion of costs for research performed by universities is, on average, comparable to if not slightly less than other research performers, such as federal laboratories and private contractors (RAND, 2000). Moreover, since 1991, the Office of Management and Budget has had in place a cap of 26-percent on the administrative expenses (including costs incurred by the university to comply with federally mandated regulations) the federal government will reimburse. In effect, if a university is spending an average of 30 cents for each dollar of federal research MTDC, it only receives 26 cents per dollar.” – Breaking Down the Costs of Federally Sponsored Research at Universities

Key Points

- What it costs to perform research is not uniform between institutions.

- F&A cost reimbursement rates vary from institution to institution because construction, maintenance, utilities, and administration costs* vary by institution and by region. A 2023 COGR F&A Survey found that of 120 respondents, 70% of private institutions were located in the Northeast or West while 57% of public institutions were located in other regions (Midwest, Southeast, Southwest).

* As recognized in the Federal General Schedules for Salaries, the cost of living and associated wage differentials vary significantly across regions. - The type of sponsored research will also affect the rate. An institution with a heavy emphasis on microelectronics requires more costly facilities than one devoted to the humanities and social sciences.

- F&A rates depend upon other factors such as the age and condition of facilities and buildings and the amount of renovation and construction needed to house certain types of research projects. For example, the F&A costs for a biomedical research facility built in an urban area that experiences earthquakes is different than an engineering research facility built in a rural area.

Examples from Institutional Websites

- “There is no single answer to this question. Instead, the main differences result from the following factors:

- The size and intensity of use of a university’s research facilities and buildings is the primary cause for variability of F&A costs. For example, if two universities have the same direct cost research base and one has twice as many net square feet of space assigned to research, the facilities rate component for the university with twice the net square footage will be much higher.

- A university’s ability to secure funds to construct, upgrade and maintain research facilities. Universities that are able to spend money to renovate existing research facilities and construct new research facilities experience a higher level of costs than universities with limited funding for such expenses.

- The location of a university has a significant effect on the costs of facility operations. The universities that have the best combination of climactic conditions, utility rates, and/or labor costs will generally have a lower rate for facility operations.

- The “mix” of research among universities contributes to the variances in facilities rates. The cost per square foot of constructing or renovating biomedical research space is more costly than the cost per square foot of space for mathematicians.” – The University of Illinois System

- “F&A cost rates can vary significantly across institutions due to differences in costs across different regions of the country, urban versus more rural environments, the type and complexity of the research portfolio of the institution, and other variables that impact the cost of doing research.” – COGR Excellence in Research: The Funding Model, F&A Reimbursement, and Why the System Works

- “F&A cost rates vary from institution to institution because construction, maintenance, utilities, and administration costs vary by institution and by region. Additionally, F&A rates depend upon other factors such as the age and condition of facilities and buildings and the amount of renovation and construction needed to house certain types of research projects. For example, the F&A costs for a biomedical research facility built in an urban area that experiences earthquakes is different than an engineering research facility built in a rural area.” – COGR Frequently Asked Questions about Facilities and Administrative (F&A) Costs of Federally Sponsored University Research

Key Points

- Payments are reimbursements for costs already paid for by the university.

- Payments for F&A reimbursements are NOT a revenue source for the university.

- Indirect costs are not a revenue stream but a cost recovery from federal research sponsors for support of the research work already performed. IDC dollars are not charged to sponsors until direct research expenditures occur.

- The federal F&A cost reimbursement process ensures only necessary, allowable expenses are reimbursed. Reimbursement may be put back into the general fund, from where the original expenses were paid. But, like a travel expense reimbursement to an individual, how the reimbursement is spent is not relevant, only the expenses being reimbursed are relevant.

- The total amount of F&A costs a university incurs is not completely reimbursed by the federal government.

Key Point to Avoid

• Statements/graphics that show F&A cost reimbursements as a revenue source. While this may be reflective of how your institution describes these reimbursements internally, it sends an inaccurate message publicly about what the funds support and undermines our ability to show universities are good stewards of federal taxpayerdollars. F&A cost reimbursements partially replenish funds the institution has already spent and do not create new money, regardless of the institution's method of budgeting and accounting for them.

Examples from Institutional Websites

• “F&A costs (also known as ""overhead"") reflect the actual cost of conducting research at Georgia Tech and are not extra money, or profit, attached to research contracts. F&A funds reimburse actual expenses Georgia Tech has already incurred to support research activities. They are real costs related to buildings, maintenance, utilities, equipment, insurance, safety, administration, compliance, legal, etc. F&A costs are collected retroactively.” – Georgia Institute of Technology• “WHAT IS ICR AND HOW CAN IT BE SPENT? As stated above, ICR is a reimbursement of expenditures to cover some portion of the indirect costs incurred as a function of completing a research award. Or, in contrast to tuition, ICR is not revenue but a repayment of costs already sustained. As such, the use of ICR funds is not restricted to any particular use. A useful analogy is the reimbursement of expenses for the business use of a personal automobile. When an employee uses her car for a business trip, the university reimburses the employee at a standard rate per mile. When the employee receives the reimbursement, she is under no obligation to use the funds for auto-related expenses. Similarly, the campus is under no obligation to use the ICR in a certain way. Instead, we choose to distribute indirect cost recovery in a way that is associated with

the research efforts of the campus.” – University of California, Davis

Key Points

- There is a 26% cap on administrative cost recovery for universities regardless of how much must be spent on administrative costs to ensure research is conducted safely, securely, efficiently, and effectively. Universities are the only federal grantee or contractor on which such a limitation on federal payment of administrative costs exists. The COGR 2023 Survey of F&A Cost Rates found that the average calculated administrative component of the 120 responding institutions was more than 9 percentage points higher than the 26% cap (35%).

- There are specific federal agencies on which statutory caps are imposed which limit indirect cost payments (e.g. U.S. Department of Agriculture). Caps on F&A payments have also been imposed by agencies on specific programs.

- Institutions make large investments in human and physical capital, and F&A cost reimbursement only pays a portion—in some cases decades later. For example, a research building needed for the types of research federal sponsors want is built. The useful life of the building is 30 years so only 1/30th of the cost is included as building depreciation in the F&A cost reimbursement rate. Then, only the portion of the 1/30th allocable to externally funded research is partially reimbursed by the research sponsors, including the federal government. The institution pays for the internally funded research that takes place in the building and the building and other F&A costs allocable to that research, and any other activities not allocable to external sponsors.

Text Examples for Institution Websites

- “OBSERVATIONS AND FINDINGS. 1. Universities are prohibited by regulation from requesting reimbursement for the full cost of conducting federally funded research and are paying an ever-increasing share of that cost. … 4. The federally mandated 26% cap on reimbursement of university administrative costs prevents universities from charging federal awards their proportionate share of the cost burden associated with the extensive growth in federal regulations since enactment of the cap in 1991.” – COGR F&A Survey Capstone: Cost Reimbursement Rates, Actual Reimbursement, and Growing Regulatory Cost Burden

- “The 26% Administrative Cap and Research Compliance Costs. In 1990, a federal audit resulted in the identification of unallowable costs in one institution’s F&A rate. Federal officials perceived the situation to be widespread and, as a result, imposed a 26% cap (via a 1991 revision of Circular A-21) on all universities’ federal reimbursement of administrative costs. Universities across the country responded by utilizing advanced technology for additional accounting system controls to ensure proper exclusion of costs not allowable for federal reimbursement. The capped rate was determined based on data representing average administrative costs at universities prior to 1991. Since then, numerous and complex compliance requirements have evolved, including but not limited to those related to human subjects protection, animal care and use, laboratory and hazardous waste safety, data security, conflict of interest, research misconduct, export controls, effort and financial reporting, and campus-wide education programs. Despite the significantly increased real administrative costs of conducting federally- funded research at universities, the administrative cap remains in effect at 26%.” – COGR 2014 Finances of Research Universities PART II. RESEARCH FUNDING AND FINANCIAL IMPLICATIONS

- “R&D Expenditures, by Type of Cost - Of the more than $108 billion in total FY 2023 R&D expenditures, higher education institutions identified $84.2 billion in direct costs and $24.5 billion in indirect costs (figure 2). … Among indirect costs, $17.7 billion of facilities and administrative costs were reimbursed from external R&D sponsors. Another $6.8 billion was identified as unrecovered indirect costs.” – NSF NCSES InfoBrief, Higher Education R&D Expenditures Increased 11.2%, Exceeded $108 Billion in FY 2023

Source: University of Cincinnati

Source: University of Cincinnati

Data View

| Type of cost | R&D expenditures |

|---|---|

| All costs | 108,681 |

| Direct costs | 84,209 |

| Salaries, wages, and fringe benefits | 47,089 |

| Software purchases | 222 |

| Capitalized equipment | 3,260 |

| Passed through to sub-recipients | 9,515 |

| Other direct costs | 24,122 |

| Indirect costs | 24,473 |

| Recovered costs | 17,702 |

| Unrecovered costs | 6,771 |

- FAQ and Issue Briefs

- Visual Content

- Association Websites

- Other Key Reports/Documents

- Hearing on the Role of Facilities and Administrative Costs in Supporting NIH- Funded Research, October 2017

- Hearing on Examining the Overhead Cost of Research, May 2017

- “Analysis of F&A at Universities,” WH OSTP, 2000

- “Paying for University Research Facilities and Administration,” RAND, 2000

- “History of Indirect Cost Policies,” Congressional Research Service (CRS), 1994

{kind=link}

Want more information on grants and sponsored research at Belmont?

Email osp@belmont.edu or contact

Ellen Zinkiewicz

Director of the Office of Sponsored Programs

ellen.zinkiewicz@belmont.edu | 615.460.5721

Brenda Gill

Grants Adminstrator

brenda.gill@belmont.edu | 615.460.5814

If you are a student interested in conducting research or applying for a grant with a faculty member, please consult your major professor or faculty advisor.

BRIDG Grants

The Belmont Research & Innovation Development Grants program offers micro-grants of $500–$3,000 to faculty and staff pursuing innovative ideas, pilot projects and early-stage research. BRIDG grants catalyze new initiatives aligned with Belmont's mission, fostering creativity, discovery, and continuous improvement across campus.